Unpublished financial statements can cost a company hundreds of thousands of Czech crowns, complicate access to financing and, in extreme cases, even lead to the dissolution of the company. Despite this, thousands of Czech companies ignore this statutory obligation every year. Some managing directors consider it a minor administrative lapse. The opposite is true – it is a legal obligation with specific sanctions, and last but not least, it is also a signal that partners, banks and investors perceive very negatively.

Who is subject to the disclosure obligation?

In the Czech Republic, the obligation to disclose financial statements in the Commercial Register applies, in principle, to all business corporations – i.e. limited liability companies, joint-stock companies, limited partnerships and general partnerships. The obligation also applies to cooperatives and to branches of foreign entities registered in the Commercial Register. Financial statements are disclosed to the extent corresponding to the category into which the business corporation falls.

The law stipulates a specific deadline: the financial statements (if subject to audit, then the audited financial statements) must be filed in the Collection of Documents of the Commercial Register within 30 days of their approval by the general meeting, but no later than 12 months from the balance sheet date of the relevant accounting period. This means that even where the general meeting does not approve the financial statements or does not take place at all, the obligation arises to disclose them no later than one year after the end of the accounting period.

Why do companies not disclose their financial statements?

The reasons vary. In practice, we most often encounter the following:

- Lack of awareness or underestimation of the obligation. Particularly in smaller limited liability companies, there is a belief that if the company does not exceed the thresholds for a mandatory audit, the disclosure obligation does not apply. This is incorrect – the obligation to disclose and the obligation to audit are two completely different obligations.

- Concerns about publishing financial results. Statutory bodies and owners argue that they do not want competitors, customers or employees to be able to view the company’s financial performance. This motivation is humanly understandable, but from a legal perspective it does not lead to a correct solution.

- Administrative overload. Financial statements are not prepared in time, the general meeting is postponed, and the documents are not filed on time.

- Intentional concealment of information. The most serious case, where the company deliberately conceals information about its financial performance – for example in disputes between shareholders, in pre-insolvency situations or in other irregular circumstances.

What sanctions may be imposed?

Czech legislation links failure to comply with the disclosure obligation with several types of penalties.

Fine imposed by the registry court

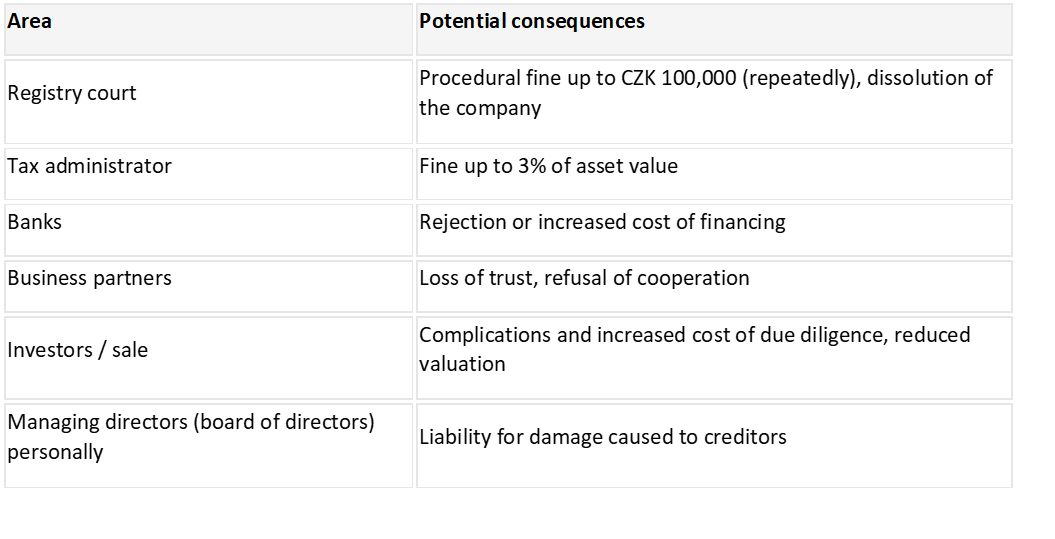

A registry court may impose a procedural fine of up to CZK 100,000 on a company that fails to disclose its financial statements. The court may do so repeatedly. In practice, this sanction has not been imposed automatically; however, following the introduction of automated monitoring of compliance by registry courts, the situation is changing and the number of fines imposed is increasing.

Fine imposed by the tax administrator

The tax administrator also has the authority to impose a fine – potentially even a higher one, as the Accounting Act provides for a sanction of up to 3% of the value of a company’s assets in the case of serious breaches of accounting regulations. Failure to disclose financial statements constitutes a breach of the Accounting Act and may fall under this regime. Particularly in the case of large accounting entities, the fine may therefore be significant.

Dissolution of the company by the court

This is the most serious consequence, of which many managing directors are unaware or believe cannot occur. The Business Corporations Act gives the registry court the authority to initiate proceedings for the dissolution of a company if it repeatedly fails to comply with statutory obligations – and failure to disclose financial statements is explicitly listed in the law as one of the reasons. The court will usually first call on the company to remedy the situation and set a reasonable deadline, but if the company still fails to comply, it may proceed to dissolve the company with liquidation.

Liability of the statutory body

The obligation to disclose financial statements primarily rests with the company’s statutory body (in the case of a joint-stock company, the board of directors; in the case of a limited liability company, the managing directors). If the statutory body knowingly and over a prolonged period ignores this obligation, it exposes not only the company to sanctions, but also itself to liability for damages caused to creditors or third parties, especially in situations where it turns out that concealed financial results would have influenced their business decisions.

Impacts that cannot be quantified by a fine

Legal and financial sanctions are only one dimension of the problem. There are many others that may be even more economically significant for the company.

- Banks and financing. Most banking institutions require up-to-date financial statements when assessing a loan application or reviewing existing financing. Missing financial statements in the register are an automatic warning signal and may lead to rejection of the loan or tightening of its terms.

- Business partners and due diligence. As part of standard business practice, reputable partners verify new suppliers and customers. Missing financial statements or financial statements published with a delay of several years are grounds for caution and sometimes for refusing cooperation.

- Public procurement. Bidders for public contracts are typically required to demonstrate economic capability. Unpublished financial statements may be an obstacle to meeting qualification requirements.

- Investors and sale of the company. In any equity investment or sale of a share, potential investors carry out detailed due diligence. Missing or delayed financial statements prolong and increase the cost of the entire process and may lead to a reduction in the purchase price or to the termination of the potential investor’s interest.

How to remedy the situation?

If a company finds that it has not disclosed its financial statements for previous years, the solution is straightforward: file the missing financial statements in the Commercial Register as soon as possible. Neither the law nor the practice of registry courts is generally hostile to voluntary remediation – the key is to actively address the situation rather than wait for a court notice.

When filing financial statements for multiple years retrospectively, it is appropriate to:

- verify that approved financial statements are available (minutes of the general meeting or a decision of the sole shareholder), and in the case of an audit obligation also evidence of approved audited financial statements,

- prepare the financial statements in the legally prescribed format (XBRL format for larger accounting entities),

- file everything in the Collection of Documents of the Commercial Register via the website www.justice.cz,

- and in the case of extensive delay, consider communication with the registry court.

Conclusion or summary of impacts in case of non-disclosure of financial statements

Area

Disclosure of financial statements is not just a bureaucratic formality. It is a fundamental condition of transparent business, protecting creditors, business partners, as well as the company itself and its management. If you are unsure about the status of compliance with this obligation or need assistance in remedying past shortcomings, contact our specialists – we will be happy to help you resolve the situation.

This text was translated by AI.

Authors

-

-

Renata Emmer

Renata Emmer works as audit manager. She specialises in audit of production, trading and leasing companies, transformation of financial statements compiled according to the IFRS or other international accounting standards. Her current portfolio of clients includes a number of various companies, including hotels, real estate companies, engineering, trading and production companies.View Profile